Recently, we conducted a poll on LinkedIn to find out what you thought about the following question: do you have to pay crypto tax? The results were fairly split, so we decided to clear up any misconceptions you may have!

Like any other investment, cryptocurrencies have their own tax implications. In some cases, investors can deduct capital losses from their income. But when it comes to crypto taxes, it can be difficult to separate fact from fiction.

In this article, we’ll be outlining exactly how crypto tax affects the mysterious world of cryptocurrency. By the end of it, you’ll understand how to stay in line with UK legislation on crypto tax.

Do you have to pay crypto tax?

To put it simply – yes; crypto is subject to taxation in the UK. However, there are some exceptions in how crypto tax differs from the norm.

Firstly, crypto falls under the same class as a property or asset. Therefore, they are similar to shares in how taxation affects them.

When dealing with crypto, you’ll most likely face either income tax or capital gains tax. This depends entirely on how you classify your trading. Income tax will cover business activities, whilst your own investments will generally fall under capital gains tax.

Any disposal of crypto will render you liable to taxation. To define this, disposal is classed as selling, exchanging or using crypto in any way that results in financial gain.

When do you have to start paying crypto tax?

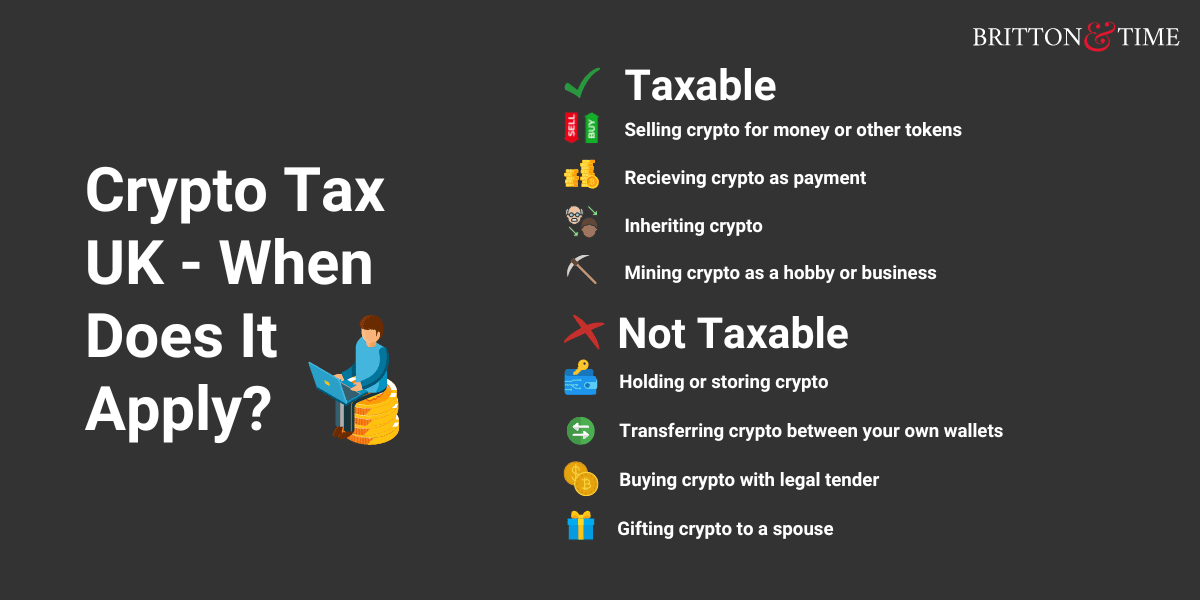

There are a number of activities that will result in you having to pay crypto tax. These include:

Buying and selling crypto – profiting off of your crypto means you’ll likely have to pay capital gains tax. If you make a loss, this could minimise your capital gains bill. However, the first £12,300 you earn per year is not taxed.

Being paid with crypto – receiving payment in crypto means that you’ll be subject to income tax and national insurance. The amount of income tax you pay will be determined by which tax bracket you are in, as detailed further down the article.

Inheritance – as crypto is technically property in the UK, it is subject to inheritance tax. This means that if the estate is worth over £325,000, a tax fee will affect any amount that exceeds this limit. For example, if you are due to inherit £500,000 worth of crypto, you’ll be taxed 40% of £175,000 (£70,000).

Mining crypto – when mining crypto as a business, any income made is taxable as it falls under trading profit. This also applies to any gains made when disposing of your cryptocurrency too. On the flip side, mining as a hobby is slightly different. If you receive an income or a reward for mining, these will both be subject to crypto tax. Later down the line, when disposing of assets, you’ll be subject to capital gains tax too.

When am I not subject to crypto tax?

It is true that most crypto-related activities will result in taxation. However, simply handling crypto isn’t enough to result in taxation.

Some examples of where crypto tax does not apply include:

- Holding crypto

- Transferring crypto between your own wallets

- Buying crypto with fiat currency i.e. legal tender

- Gifting crypto to a spouse

In essence, if you are not directly earning or gaining, then crypto tax does not apply to you.

What about airdrops?

Airdrops are essentially free tokens sent out to try and entice recipients into engaging with the crypto. For example, you may receive a crypto token for following a social media account, or signing up for updates on their website.

These work in the same way as promotional vouchers sent to your email. In both cases, they are trying to bring new customers in.

In the UK, airdrops do not require you to pay crypto tax. However, if you later down the line decide to dispose of the token, you may be subject to capital gains tax.

Can the HMRC track crypto exchanges?

Yes – they can. As crypto can be bought and disposed of on centralised and decentralised exchanges, it works slightly different in how the HMRC will track your taxable income.

On a centralised exchange, the HMRC is informed of your wallet identity via a KYC check – which stands for Know Your Customer. This works in a similar way to trading stocks, and essentially tells them of any gains you make from handling crypto. This means any exchanges made are traceable.

Decentralised exchanges are harder to track however. Customers using such exchanges are the only ones that have access to their wallets and keys, thus making it harder for any authorities to track their activity.

Despite this, you will eventually have to transfer your crypto back into fiat currency (i.e. legal tender), meaning that the HMRC will look into any amount they deem suspicious. Therefore, you should always keep track of your transactions even when exchanging on a decentralised platform, in order to adhere to tax regulations.

What about swapping cryptocurrencies?

If you decide to simply swap between cryptocurrencies, you are still liable to taxation as it is still considered as a disposal. Even though you are exchanging for a different token, you may be profiting from what the original value of your cryptocurrency was worth.

Here’s an example…

Let’s say that, in January, you decide to buy some Binance Coin when it’s worth £200. Later in the year, come September, you decide to swap it for Tether. However, at this point in time, the price of Binance Coin has risen to £220. Because of this, you’ll now be receiving a 10% increase in Tether purely because of the increasing price of Binance Coin.

Whilst in this example the price increase wasn’t massive, regular occurrences or a one-off large swap will definitely be liable for taxation. Because of this, it’s vital to keep records of all disposals for crypto tax purposes.

You won’t be liable to taxation if you haven’t exceeded your yearly capital gains tax allowance of £12,300. This is includes any disposal of crypto, whether it be for another token or for fiat currency.

How can I calculate my financial gain?

To account for the ever-fluctuating nature of crypto, there a series of rules in place to help calculate the ‘true’ value of your trades. The implementation of such rules are purely to cover any bases where people can avoid paying tax. These are:

The ‘same-day’ rule

Any cryptocurrencies or tokens acquired or disposed of on the same day will fall under one transaction. This groups them together to work out an average cost or amount received through the trade.

This means that the costs for any sales you make will be the same cost as when you first acquired the crypto. This is true as long as it all occurred on the same day.

The ‘30-day’ rule

Any cryptocurrencies or tokens acquired or disposed of in the last 30 days will fall under one group to work out the average cost. This only applies when the previous rule is not valid.

The ‘pooling’ rule

When the previous rules cannot be applied, all crypto bought must be put into a group with the average price worked out. This is usually due to it being unmatched by any other recent transactions.

Have a legal matter concerning crypto tax?

How much crypto tax do I pay on gains?

Crypto tax will generally fall under one of two categories – income tax or capital gains tax. These work slightly differently depending on a number of factors, which include:

- Frequency of trades

- The amount you hold or trade

- The amount of time that you hold or trade for

- If you trade under a business or commercially

As a general rule of thumb, if you are trading crypto in any shape or form, you will most likely fall under some form of UK taxation.

Income tax

Reporting profit from crypto as income will make it fall under income tax. The rates for these are the same in England, Wales, and Northern Ireland, but differ slightly for Scotland.

The rates in England, Wales and Northern Ireland are:

| Income | Taxable amount |

|---|---|

| £0 – £12,570 | 0% |

| £12,571 – £50,270 | 20% |

| £50,271 – £150,000 | 40% |

| Over £150,000 | 45% |

The first £12,570 you earn yearly will be tax-free. Anything that exceeds this amount will fall into one of the brackets above.

In Scotland, there are also starter and intermediate rates at 19% and 21% respectively.

Capital gains tax

Anyone who disposes of a cryptocurrency is subject to capital gains tax. This is because it’s considered an investment and, thus, generates a gain deemed tax worthy.

You do not have to pay capital gains tax if your trading does not result in a profit of over £12,300. Once you exceed this threshold, the amount of tax you’ll be facing depends on if you fall under basic rate or higher rate income tax. You can calculate this by visiting the government page on capital gains tax.

How can I prepare for crypto tax season?

To ensure that you have all bases covered when it comes to crypto tax, there are a number of things you need to declare. This includes:

- Type of cryptocurrency/token you hold or previously held.

- When you sold them

- The amount you sold

- Value of your currencies/tokens in GBP

- Wallet addresses

We suggest keeping track of all your crypto outgoings, alongside noting down the value of trades in GBP. It would be a nightmare to try and recall all of your crypto activity a day before you are due to report your taxes!

If you don’t wish to record these things yourself, it might be wise to consult an accountant to help you avoid any taxation fines.

We’re here to help

About the Author

Comments

Due to a near fatal car accident I'm currently and potentially may be for the rest of my life be on disabilities and universal credit.

When I received my payout I invested some money in crypto

As I am not working im confused on where I fit in as far as tax goes if I ever want to take profit

Due to a near fatal car accident I'm currently and potentially may be for the rest of my life be on disabilities and universal credit.

When I received my payout I invested some money in crypto

As I am not working im confused on where I fit in as far as tax goes if I ever want to take profit

Leave a comment Your email address will not be published.